Unfettered

View on Super

John Abernethy

In late 2020 the ‘Callaghan Review and Report into Retirement Income’ was presented to the Government. In his press release the Treasurer asserted that the Report ‘confirms the Australian retirement income system is effective, sound and its costs are broadly sustainable’.

In recent weeks, the AFR has published differing views on the efficacy of maintaining the superannuation guarantee at the current 9.5%.

First, Senator the Hon Jane Hume (Assistant Minister for Superannuation, Financial Services and Financial Technology) presented the argument (supported by the Callaghan review) that the current employer contribution rates were adequate. In response, the former Prime Minister Paul Keating unveiled a vitriolic attack on the Government position.

In presenting my view of Superannuation I can refer readers back to the opinion piece (below) that I wrote for the AFR at the height of the last election campaign when the ALP proposed to demolish Australia’s franking system.

In that piece I suggested that no changes to the superannuation or retirement system should be made until the Nation developed a desired outcome against which changes could be measured.

I suggested that a desired outcome should be “directed and measured against our Nations desire to have retired Australians living with a reasonable standard of living supported by a pension system that creates a safety net for everybody”

Therefore, I was pleased to see that the Callaghan review suggested that a clear objective for the system needed to be developed to guide policy. The review suggested the objective as – ‘to deliver adequate standards of living in retirement in an equitable, sustainable and cohesive way’.

In his attack on the Government positioning on superannuation (effectively to hold the contribution level) Paul Keating exhibited a bias in promoting the management of superannuation by predominantly union influenced large Industry Funds.

Despite being the ‘architect of superannuation’, Paul Keating’s opinion piece once again exhibited his failure to set a proper objective at the formation of the system. If he had then, he would now acknowledge that the Superannuation system hasn’t delivered much for the majority of retired Australians.

The meandering travel of super

The superannuation system and its rules have undergone numerous tinkerings since its inception. For a while (the Costello years) the changes were driven by covert pressure from the “influential and well off” (so to speak) to seek similar retirement and tax benefits that had been afforded to politicians through their excessive and unfunded retirement benefits.

Then there has been a reigning-in of contribution limits etc (both ALP and Coalition governments) to stop the excessive utilisation of taxation benefits that have nothing to do with supporting a reasonable retirement income.

However, all of the above tinkering was directed at a superannuation system that was flawed from its creation. An “account based” system that sits across a poorly structured and unfunded pension system which is showing increasing signs of both failure and inadequacy.

After 25 years, that failure, was shown by Keating’s own observation

“in 2018, men older than 75 had a median balance of $200,000, while women of the same age had $126,000”.

More disturbing was the Callaghan review observation that in June 2019,

71% of all persons over 65 of age were recipients of the National pension. Further, 42% of all pensions paid were at the maximum rate.

These observations are hardly the observation of success. Therefore it is not surprising that Paul Keating did not acknowledge its failure and therefore the urgent need to fix the system to achieve the desired outcome and to make it viable, fairer and less costly to administer.

$3 trillion does not solve the problem

It is not an issue of size. The whole system does not need more funds directed at it. Indeed with $3 trillion in assets the Australian superannuation is in totality (not individually) probably over funded. These assets represent over 150% of Australia’s GDP, and 300% of the projected size of the Commonwealth debt as we emerge from Covid19.

The growth in funds and its increasing direction to larger Industry Funds will create problems in a world corrupted by QE and zero interest rates. Could these large Industry Funds grow to have too much to invest and then suffer from the diseconomies of scale that flow from excessive capital?

The evidence suggests this and now we are seeing the warning signs as these funds increasingly drift into offshore and low yielding markets seeking out long term annuity assets that have been perverted by QE. Then there is the drift to public company takeovers, private equity and hedge fund offerings.

The Australian superannuation system is bloated and poorly designed. Australia needs a basic national contributory pension system that is not means or asset tested. If taxpayers contribute then they should rightly expect a pension in retirement. Afterall, it’s exactly what former politicians (including Paul Keating) get and many of them, prior to 2005, made no contribution.

Long term investing (accumulation) should be balanced against the constant need for the servicing of pensions inside both a Commonwealth Pension scheme and a National Retirement savings scheme.

Financial advice never more important

The financial advice community should be able to provide its services to clients with certainty, inside a sensible and logically structured national scheme. Clients should not be advised to jettison assets to qualify for a pension. That is not a good policy outcome, and one that is created by a poorly designed scheme that is failing to deliver for the majority of Australians.

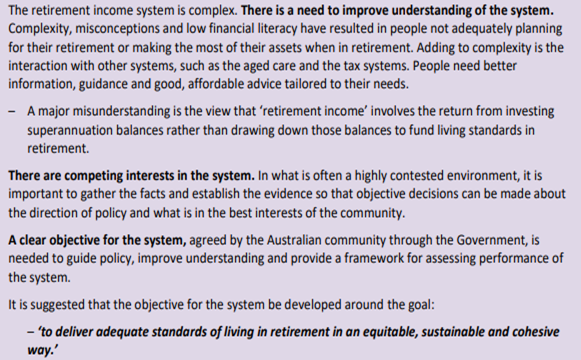

The Callaghan review made the following observations which are pertinent for financial advisers in their provision of service and education to their clients.

These observations present as quite rational and absolutely justify as to why the investing public and particularly self directed retirees, require advice.

To the contrary, the condemnation by Keating indicated a basic misunderstanding of superannuation in pension mode. As all advisers know, there is an age directed pension payment schedule. The percentage of capital value of the annual legislated pension payment increases as the beneficiary ages. At 90 years of age the rate increases to 11% per annum (half this rate during Covid). At 95 years the rate increases to 14%.

The point being that the law requires that a pension fund’s capital is exhausted as a beneficiary ages. Paul Keating’s attack on the Coalition Government’s policy to exhaust a superannuation fund at time of death is the same policy as the ALP.

When Keating designed the superannuation system he did so with no expectation that people would live into their nineties. He did not foresee a burgeoning pension system would be created in the self directed market. He did not understand that pension schemes inside super should be managed with flows to savings outside super. He did not foresee that people would want to understand as to how they can and should adapt their investments both inside and outside super. He did not understand the importance of financial literacy and advice.

It is time for an overhaul of the superannuation system that was designed 26 years ago to bring it up to date with the reality of Australia today. A proper overhaul would then allow the financial advisory community to provide logical and sensible support to their clients inside a scheme that is fit for purpose.

In this Edition:

Unfettered

View on Super

John Abernethy

In late 2020 the ‘Callaghan Review and Report into Retirement Income’ was presented to the Government. In his press release the Treasurer asserted that the Report ‘confirms the Australian retirement income system is effective, sound and its costs are broadly sustainable’.

In recent weeks, the AFR has published differing views on the efficacy of maintaining the superannuation guarantee at the current 9.5%.

First, Senator the Hon Jane Hume (Assistant Minister for Superannuation, Financial Services and Financial Technology) presented the argument (supported by the Callaghan review) that the current employer contribution rates were adequate. In response, the former Prime Minister Paul Keating unveiled a vitriolic attack on the Government position.

In presenting my view of Superannuation I can refer readers back to the opinion piece (below) that I wrote for the AFR at the height of the last election campaign when the ALP proposed to demolish Australia’s franking system.

In that piece I suggested that no changes to the superannuation or retirement system should be made until the Nation developed a desired outcome against which changes could be measured.

I suggested that a desired outcome should be “directed and measured against our Nations desire to have retired Australians living with a reasonable standard of living supported by a pension system that creates a safety net for everybody”

Therefore, I was pleased to see that the Callaghan review suggested that a clear objective for the system needed to be developed to guide policy. The review suggested the objective as – ‘to deliver adequate standards of living in retirement in an equitable, sustainable and cohesive way’.

In his attack on the Government positioning on superannuation (effectively to hold the contribution level) Paul Keating exhibited a bias in promoting the management of superannuation by predominantly union influenced large Industry Funds.

Despite being the ‘architect of superannuation’, Paul Keating’s opinion piece once again exhibited his failure to set a proper objective at the formation of the system. If he had then, he would now acknowledge that the Superannuation system hasn’t delivered much for the majority of retired Australians.

The meandering travel of super

The superannuation system and its rules have undergone numerous tinkerings since its inception. For a while (the Costello years) the changes were driven by covert pressure from the “influential and well off” (so to speak) to seek similar retirement and tax benefits that had been afforded to politicians through their excessive and unfunded retirement benefits.

Then there has been a reigning-in of contribution limits etc (both ALP and Coalition governments) to stop the excessive utilisation of taxation benefits that have nothing to do with supporting a reasonable retirement income.

However, all of the above tinkering was directed at a superannuation system that was flawed from its creation. An “account based” system that sits across a poorly structured and unfunded pension system which is showing increasing signs of both failure and inadequacy.

After 25 years, that failure, was shown by Keating’s own observation

“in 2018, men older than 75 had a median balance of $200,000, while women of the same age had $126,000”.

More disturbing was the Callaghan review observation that in June 2019,

71% of all persons over 65 of age were recipients of the National pension. Further, 42% of all pensions paid were at the maximum rate.

These observations are hardly the observation of success. Therefore it is not surprising that Paul Keating did not acknowledge its failure and therefore the urgent need to fix the system to achieve the desired outcome and to make it viable, fairer and less costly to administer.

$3 trillion does not solve the problem

It is not an issue of size. The whole system does not need more funds directed at it. Indeed with $3 trillion in assets the Australian superannuation is in totality (not individually) probably over funded. These assets represent over 150% of Australia’s GDP, and 300% of the projected size of the Commonwealth debt as we emerge from Covid19.

The growth in funds and its increasing direction to larger Industry Funds will create problems in a world corrupted by QE and zero interest rates. Could these large Industry Funds grow to have too much to invest and then suffer from the diseconomies of scale that flow from excessive capital?

The evidence suggests this and now we are seeing the warning signs as these funds increasingly drift into offshore and low yielding markets seeking out long term annuity assets that have been perverted by QE. Then there is the drift to public company takeovers, private equity and hedge fund offerings.

The Australian superannuation system is bloated and poorly designed. Australia needs a basic national contributory pension system that is not means or asset tested. If taxpayers contribute then they should rightly expect a pension in retirement. Afterall, it’s exactly what former politicians (including Paul Keating) get and many of them, prior to 2005, made no contribution.

Long term investing (accumulation) should be balanced against the constant need for the servicing of pensions inside both a Commonwealth Pension scheme and a National Retirement savings scheme.

Financial advice never more important

The financial advice community should be able to provide its services to clients with certainty, inside a sensible and logically structured national scheme. Clients should not be advised to jettison assets to qualify for a pension. That is not a good policy outcome, and one that is created by a poorly designed scheme that is failing to deliver for the majority of Australians.

The Callaghan review made the following observations which are pertinent for financial advisers in their provision of service and education to their clients.

These observations present as quite rational and absolutely justify as to why the investing public and particularly self directed retirees, require advice.

To the contrary, the condemnation by Keating indicated a basic misunderstanding of superannuation in pension mode. As all advisers know, there is an age directed pension payment schedule. The percentage of capital value of the annual legislated pension payment increases as the beneficiary ages. At 90 years of age the rate increases to 11% per annum (half this rate during Covid). At 95 years the rate increases to 14%.

The point being that the law requires that a pension fund’s capital is exhausted as a beneficiary ages. Paul Keating’s attack on the Coalition Government’s policy to exhaust a superannuation fund at time of death is the same policy as the ALP.

When Keating designed the superannuation system he did so with no expectation that people would live into their nineties. He did not foresee a burgeoning pension system would be created in the self directed market. He did not understand that pension schemes inside super should be managed with flows to savings outside super. He did not foresee that people would want to understand as to how they can and should adapt their investments both inside and outside super. He did not understand the importance of financial literacy and advice.

It is time for an overhaul of the superannuation system that was designed 26 years ago to bring it up to date with the reality of Australia today. A proper overhaul would then allow the financial advisory community to provide logical and sensible support to their clients inside a scheme that is fit for purpose.